Commissions–Annuities are generally sold by insurance brokers who charge a fee of anywhere from 1% for the most basic annuity to as much as 10% for complex annuities indexed to the stock market. In general, the simpler the annuity structure or the shorter the surrender charge period, the lower the commission. For example, a variable annuity with a 10-year surrender charge period will pay a higher commission than one with a 5-year surrender charge, which results in a higher commission fee for the investor.

How To Calculate The Value Of An Annuity

As with any major financial decision, consulting with a financial advisor can help you better understand how a fixed annuity can fit into your investment strategy. A financial advisor can provide you with personalized recommendations and information about fixed annuities and other products that may be beneficial to you. The purpose of this calculator is to compute the future value of a series of deposits. This is an investment or saving account and, you are calculating the accumulation of a series of deposits, the annuity payments, and what the total value will be at some time in the future.

Running Out of Money in Retirement: What’s the Risk?

It is only possible to calculate with certainty the value of a fixed-rate annuity. By definition, the payments made by variable annuities and indexed annuities can potentially change over time. But let’s take a look at how the future and present values of these annuities are typically calculated.

Using the TI BAII Plus Calculator to Find the Future Value for Annuities Due

- The future value of annuity calculator is a compact tool that helps you to compute the value of a series of equal cash flows at a future date.

- Suppose you are considering entering into a data plan for your smart phone that will cost you $35 per month.

- The time period may be a fixed period, such as 20 years, or perhaps for the rest of the client’s life.

- Moving the slider to the left will bring the instructions and tools panel back into view.

- The majority of annuity investments are made by investors looking to ensure that they are provided for later in life.

See how different annuity choices can translate into stable, long-term income for your retirement years. The bottom line is, the only way to make wise financial decisions is to be able to accurately weigh what you are giving up in exchange for what are there taxes on bitcoins you are getting. Understanding annuities (and other Time Value of Money principles) is critical to that process. And that’s only considering just one of the possible hundreds of the non-essential expenditures you likely make on a regular basis.

Best Annuity Products of 2024

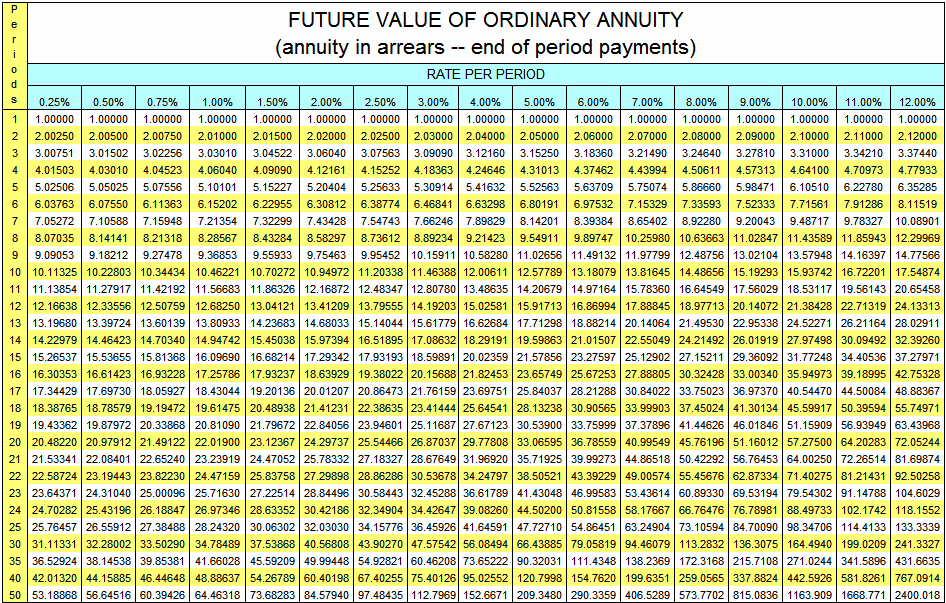

A Data Record is a set of calculator entries that are stored in your web browser’s Local Storage. If a Data Record is currently selected in the “Data” tab, this line will list the name you gave to that data record. If no data record is selected, or you have no entries stored for this calculator, the line will display “None”. Calculate the future value of an annuity for either an ordinary annuity, or an annuity due.

Future Value of an Annuity with Continuous Compounding (m → ∞)

To account for payments occurring at the beginning of each period, the ordinary annuity FV formula above requires a slight modification. The understanding of future value, both for lump sums and for annuities, is absolutely critical to making financial decisions that will serve to maximize the emotional returns on the money you earn. Present value calculations can be complicated to model in spreadsheets because they involve the compounding of interest, which means the interest on your money earns interest. Fortunately, our present value annuity calculator solves these problems for you by converting all the math headaches into point and click simplicity. The Present Value of Annuity Calculator applies a time value of money formula used for measuring the current value of a stream of equal payments at the end of future periods. In order to determine whether an investment in a given annuity will be beneficial, you will need to learn how to calculate the present value of an annuity.

If you are struggling to make sense of the various types of annuities, some high-level guidance may be useful. Regarding risk exposure, fixed annuities are the safest, offering a fixed rate of return. Fixed-indexed annuities are potentially more lucrative, but can exhibit some volatility. Variable annuities are the riskiest type of annuity and can expose you to capital losses.

Additionally, knowing how to calculate the future value of an annuity will be advantageous for anyone who wants to achieve a variety of financial goals. With an ordinary variable annuity, the owner will be able to choose which securities they are indirectly invested in. Usually, this means variable annuities will pay out more when markets are thriving and less when markets are weak. Variable annuities are similar to fixed annuities—the annuitant pays in during the accumulation period with the promise of receiving periodic cash flows in the future.

The annuity is fully taxable income, when you receive an annuity you are actually purchasing an asset and it is a taxable income. The annuity due is paid at the beginning rather than the end of each time period. The effect of the discount rate on the future value of an annuity is the opposite of how it works with the present value. With future value, the value goes up as the discount rate (interest rate) goes up. But if you want to figure out present value the old-fashioned way, you can rely on a mathematical formula (with the help of a spreadsheet if you’re comfortable using one).